Welcome to How To Start Investing!

Welcome to our quick start guide for investing! This will be a short and sweet article about how to open your first investment account, fund it, and pick your first investment! The whole process can probably be completed in about two hours (not including researching investments).

Let’s begin!

Choosing Your First Account

There are two main categories of brokerage accounts. First, there is a traditional brokerage account with no tax benefits. And secondly, there is the traditional IRA and the Roth IRA (aka, brokerage accounts with tax benefits). If you’re aware of the differences and know which type of account you want, scroll down to the next section.

Before you go ahead and open your first account you’ll first want to decide which type of account you want. As I mentioned before, there’s a couple different ones:

- Brokerage account (basically any major investing platform you can think of has one of these accounts)

- Traditional IRA (contribution limit and tax benefits)

- Roth IRA (contribution limit and a different kind of tax benefits)

Real quickly I’ll discuss the differences and similarities of a traditional IRA and a Roth IRA.

Both IRAs have a contribution limit of $6,000/year, but if you’re young, you probably won’t hit this limit unless you’re making bank. And if you are making that kind of money at 17 you probably know more about this than I do.

Traditional IRA

Now here’s where it gets a little tricky. A traditional IRA lets you deduct any of your contributions from the same tax year in which you made those contributions. If you deposited $500 in your regular IRA in 2020, you could deduct $500 from your taxes in 2020. That seems pretty cool, but unfortunately, any withdrawals are treated as taxable income. That means when you’re in retirement and ready to start withdrawing from the account you’re taxed on that money. Say you’re 65 years old and withdraw $50,000 for a year’s spending. You’ll be taxed on that $50,000 at the same rate as if you were working. And it’s a high tax rate, it ranges anywhere from 10-37%.

People who invest in a traditional IRA are “betting” that tax rates will go down or that they’ll be in a lower tax bracket in the future. This makes the traditional IRA a better deal right now.

Roth IRA

A Roth IRA is very similar except that when you deposit $500, you don’t get to deduct that from your taxes. You’ll still have to pay taxes on that $500 at the end of the year. The upside though is that any withdrawals in retirement are completely tax-free. The people who invest in a Roth IRA are “betting” that tax rates will be higher in the future, so they would rather pay taxes now.

To be completely transparent, I personally have a Roth IRA and believe it’s the better of the two IRAs. I would rather pay taxes on $6,000 now when I’m in a lower tax bracket, than pay taxes on my $50,000 withdrawals in retirement and when I’m in a much higher tax bracket.

PLUS, once my money is in my Roth IRA, all the growth my investments experience are completely tax-free!

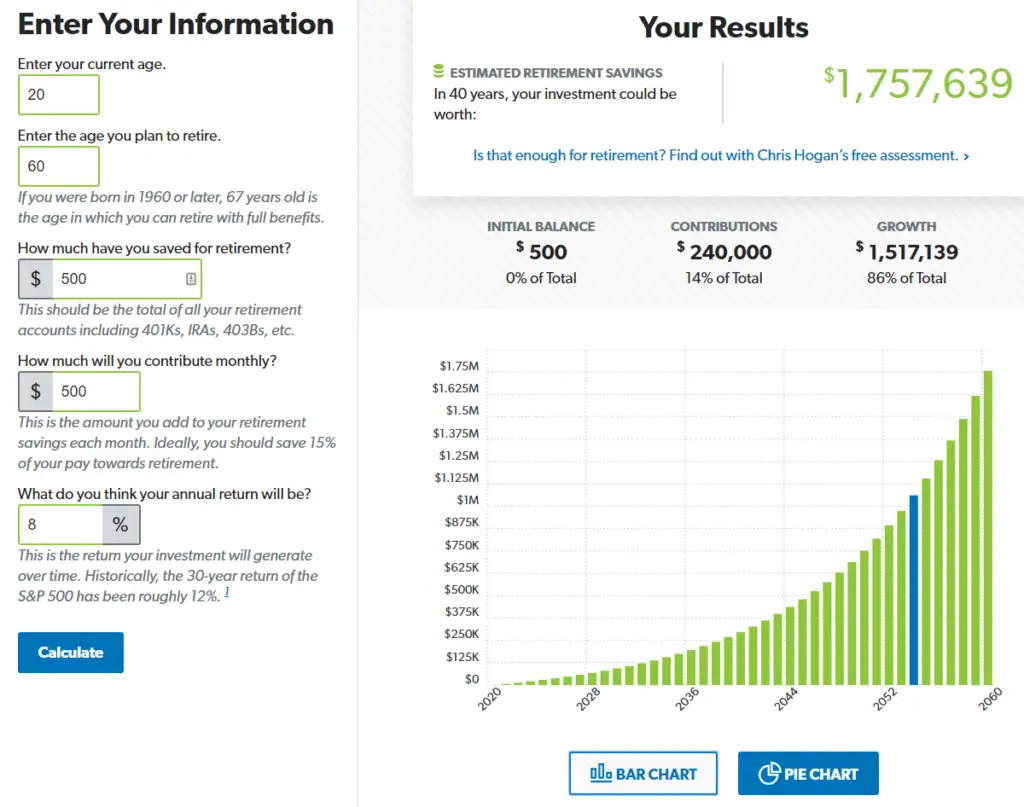

Look at it this way. If I maxed out my IRA every year from the age 20 to 60, I would retire with over $1.7 million dollars! I would rather have that money in a Roth IRA where I paid taxes on my $240,000 of contributions but the growth of $1,517,139 can be withdrawn completely tax-free.

The alternative is using a traditional IRA as my investing vehicle and being able to deduct $240,000 from my taxes in various years, but I would have to pay taxes on anything I withdraw…. the entire $1,757,639.

This is a simplified assessment of the pros/ cons of a traditional IRA or a Roth IRA, but I hope this helps you make a decision between the two accounts.

In summary…

You have three main choices: A brokerage/classic investing account, a traditional IRA, and a Roth IRA. Personally, I have two or three regular brokerage accounts and a Roth IRA. Here’s what I would recommend for different scenarios:

- If you’re looking for simplicity, speed, and a clean user interface, choose a regular brokerage account.

- If you’re looking for the best benefits, choose a Roth IRA or a traditional IRA (I would choose the Roth).

- And, if you’re money savvy nerd and want to geek out, do both! Choose an IRA of your choice and max it out every year (that would be $6,000). Then, if your income allows for it or if you’re wanting to invest even more, open a regular brokerage account and save even more money there.

I wish I could say the latter is what I’m doing now, but alas, I’m not making much money… yet.

Setting Up Your First Brokerage Account

The nice thing about a regular brokerage account is that they are SUPER easy to set up. Moreover, they have some of the cleanest UI and software out there. I have a Roth IRA with TD Ameritrade and in my personal opinion, the software is butt ugly.

What You’ll Need to Setup Your Brokerage Account

The information you’ll need will vary from brokerage to brokerage, but generally you should have this at the ready:

- Full name (hopefully you can remember that 😂)

- Phone number

- Email address

- Physical mail/home address

- Social security number

- A password manager to save your login info and security questions/answers

- Checking or saving account information (account number and routing number)

- Credit or debit card

The last two are for funding the account when you set it up. The policies on funding also vary, but depending on who you open your account with, you may be required to make an initial or minimum deposit. If you’re 18 or older the whole process will be a breeze. You could probably go from start to finish when setting up your first investment account in under an hour.

If you’re under the age of 18, alas, the process isn’t that easy. You’ll definitely need a parent with you as there will be several questions that you’ll need their help with. Also, you need their info to set up your account.

Random Note About Brokerage Firms

There are dozens of different companies you could choose, and there’s fierce competition between them. This makes it even harder to choose. A great example of this is when Charles Schwab did away with all their trading fees, taking Robinhood head-on. (Robinhood has fee-free trading.) This forced TD Ameritrade, a giant in the space, to come out with fee-free trading as well, which severely impacted their revenue. Charles Schwab stepped in shortly afterwards and acquired TD Ameritrade.

TD Ameritrade became more attainable after Schwab cut equity trading commissions to zero in October, prompting Ameritrade and other brokers to eliminate commissions, too. While the stocks of both firms were already down sharply due to the Federal Reserve’s interest-rate cuts, Ameritrade stock fell an additional 26% after the commission cut. That further stock-price decline opened the door for Schwab to swoop in and buy the company without paying an equity premium for the trading revenue that it had helped to wipe out.

Barron’s

Anyways, sorry I got a little sidetracked there. I just thought that it was a fascinating story. 😄

Best Brokerage Accounts (for those 18 or older)

Below are some of the top brokerage accounts in my opinion, based on ease of use and UI, lowest possible fees, and simplicity.

- Robinhood: A very popular choice. As soon as I turn 18 I’m setting up an account here to see what I think.

- Webull: A very close contender with Robinhood. If you’d like to check it out without signing up, click here

- M1 Finance: I am also thinking about setting up an M1 Finance account. They offer free automated investing as well as checking accounts and a debit card)

- Public: A new platform I hadn’t heard of until recently. Very nice features and slick interface. They offer a very social aspect to investing that I haven’t seen anywhere else.

- Charles Schwab: Schwab says that you can have an account set up in 10 minutes

- TD Ameritrade: I might have called their dashboard butt ugly, but I still like them. They also have some of the most robust stock research and investing practice software around known as Think Or Swim.

- Fidelity: another great choice, very similar to Ameritrade and Schwab

Best Brokerage Accounts (for those under the age of 18)

To setup a brokerage account as a minor, your parent needs to have an account with the same institution. Although, they don’t need to deposit any money themselves into that account (unless it has required minimums). These are the best companies to set up an account with as minors and parents.

- Stockpile (number one on this list is definitely Stockpile, without a doubt)

- TD Ameritrade (a solid firm but the application and account setup process is a little bit of a hassle)

- Charles Schwab (I’ve never setup an account with them, but I would assume it’s similar to TD Ameritrade

- Fidelity (also never had an account with Fidelity, but they are a behemoth in the investing space).

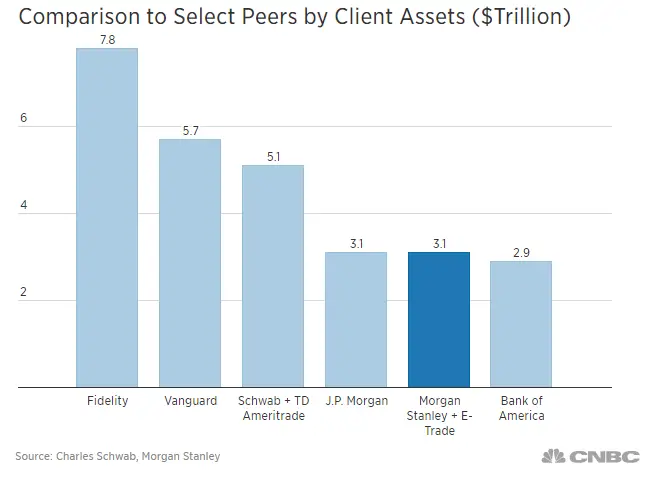

This is a quick chart of the assets under management by the biggest firms.

Setting Up Your First IRA

For the last little bit we’ve looked at different kinds of brokerage accounts for those under and over the age of 18. Here, we’ll do the same except we’re looking at the best firms to open traditional and Roth IRAs up with for both minors and those over the age of 18.

Once you’ve picked which type of IRA you would like to go with, refer to the list bleow to pick the company you would like to work with.

Best Retirement Accounts (for kids, teens, and adults)

M1 Finance

M1 Finance ranks top on my list of IRA providers due to the fact that they have a very clean interface, have the power of retirement accounts, brokerage accounts, checking accounts, and debit cards, plus zero fees. If you’re under the age of 18 though, you won’t be able to create an account.

Webull

Unfortunately, Webull is only available for those 18 years old or older and they do not offer custodial accounts for minors. They do have a very clean interface, no fees, and offer Traditional, Roth, and Rollover IRAs. Robinhood is one of their closest competitors and they both have very similar features, except Robinhood does not offer retirement accounts.

TD Ameritrade

TD Ameritrade is a solid firm and where my parents and I all have our IRAs. It’s been several years since I’ve opened my account with them so I can’t remember the entire process very well, but I don’t believe it was too difficult. My parents and I were able to get every set up fairly quickly.

Do be aware though that the software can be a bit confusing. Check out my story explaining why, below. 👇

Charles Schwab

I don’t personally have an account with Schwab but they are a great company and advertise on their site that you can get an account set up in around 10 minutes! If you’re a teen (minor), your parent could get their account set up in 10 minutes, and probably have yours set up as well in another 10-15 minutes.

Fidelity

The only reason I rank Fidelity last on this list is because I really just don’t know much about them. Like Schwab and Ameritrade, Fidelity is a great firm and has competitive features.

My Thoughts & Summary

If I was able to I would open my Roth IRA with M1 Finance, as I just really value a clean and simple experience combined with features. I find the older firms software confusing and cluttered. Close behind would be Webull, as it offers very similar things but lacks fractional shares and a checking account.

Second, it’s a toss up between TD Ameritrade and Schwab…. they’re extremely similar, but if I had to choose I would probably pick Ameritrade as I’m already familiar with them.

In third place I rank Fidelity but this is only because, A) I’ve never dealt with them or seen very much about them, and B) Their website looks ancient and that doesn’t give me very much hope for a modern investing dashboard. 😆

If you’re 18 years old or older, any of these firms and many others will work just fine for setting up any kind of IRA. Unfortunately, if you’re a minor only a few select firms offer custodial accounts. I know for a fact that Ameritrade does, and I’m 99.99% sure that Schwab and Fidelity do as well. Stockpile offers custodial accounts but not IRAs. Webull, Robinhood, Public, and M1 Finance do not allow minors to have any kind of accounts with them.

If you’re a minor trying to pick a firm to open an account with, ask your parents if they have any investing accounts currently opened. If they already have a brokerage account or an IRA with Ameritrade, Schwab, Fidelity, or another firm that offers custodial accounts, I highly recommend opening your account within the same company.

Say one of your parents has an account with Schwab. Instead of asking them to create a new account for themselves at Fidelity just to set you up an account there (unless it has some kind of major benefit), you would be better off asking them to create a custodial account for you with the same firm they’re using, Schwab.

If you’re a minor and your parents don’t have an account with a firm that allows custodial accounts, I highly recommend checking out Stockpile. I’ll let you check out their website for more details. Note: I personally have a Stockpile account and LOVE it.

So those are my thoughts on choosing a brokerage firm, but before I wrap up, here’s a quick story:

A Quick Story

The reason I stress a modern and updated UI and investing experience to be considered when picking a firm to invest with is because I have had painful experiences due to a confusing layout. I vividly remember this one evening when my parents were rushing around making supper in the kitchen. Sitting at my desk, logged into my TD Ameritrade account, browsing around, I had some money deposited and wanted to buy an index fund. I can’t remember if I “asked” for help or not, but I tried to figure it out myself.

I was on the buy page of Ameritrade and staring at the two little boxes I had to fill out. “Does this one mean I want to buy 2 shares, or $2? What do I put in this other box?”

So I took my best guess….

and I bought $2 of an index fund for a $50 fee. OUCH.

I looked at my dashboard and saw I was holding $2 of my index fund of choice, but was also $50 poorer. After diving into the depths of their website and doing some research, I figured out that if I bought a specific type of mutual fund or index fund, there would be a $50 fee every time I bought or sold it. Man, that hurt.

I ended up doing it right the second time. I put a few hundred dollars into an index fund, but I don’t remember all the details.

So that’s why I’m really fond of well designed software. 😄

The Takeaway

Those are the basics, and we’ve just begun to discover the tip of the iceberg in this article. Unfortunately, I can’t discuss every topic of investing in just one article or post, as that would probably be humongous. This is a great start though! If you’re new to the world of personal finances and are interested in investing, hopefully, this article pointed you in the right direction and helped you make a decision.

Have questions? Drop a comment below and I’ll make sure to get back to you as soon as I can!

If you’ve got your account set up and ready to go and you just need to do some research and pick your investments, check out this article we wrote on Best Stocks For A Teenager To Invest In. Also, check out the book, “Teen Investing: The Ultimate Guide to Teenage Investing.”