Welcome to this post on the case for applied financial literacy education by David R. Buten & Timothy A. Lambrecht!

Research on financial literacy education shows it can be effective if…

Much progress has been made over the past two decades towards the goal of providing financial literacy education for all high school students. The need was obvious: the end of defined benefit pension plans, the growth of increasingly complex financial products and alarming student debt burdens had created a perfect storm of financial challenges an entire generation was ill-equipped to weather. As support for the idea grew, a majority of states began to include financial literacy standards in their core curriculum, and some states began mandating a class in financial literacy in order to graduate.

The financial crisis created a greater sense of urgency as the true cost of financial illiteracy became evident. By spring of 2020 the Council for Education’s (CEE) semi-annual Survey of the States found that 21 states now require a course in financial literacy education. Despite these efforts challenges remain. The CEE reports that nearly ¼ of millennials spend more than they earn, and more than 2/3rds of Gen Y have less than three months of expenses saved in an emergency fund.

The most recent meta-analysis(1) of the effectiveness of financial literacy education, the 2020 Financial Education Affects Financial Knowledge and Downstream Behaviors from the National Bureau of Economic Research concludes that “financial education treatment effects from RCTs have, on average, positive effects on financial knowledge and behaviors”. In addition, the authors found that treatment effects were comparable or even larger than comparable effects of teaching other subjects like math or reading. That’s good news and supports our belief that effective financial education can have significant, long-lasting, and life-changing impacts on young adults.

An analysis of the research finds significant differences in the effectiveness of different financial literacy interventions as well as a decay in the effectiveness of the interventions on both knowledge and behavior over time. This is consistent with earlier research that proposed that financial literacy education is most effective when there is no time gap between when the material is learned and when it can be applied. One of the studies cited specifically compared active learning with traditional lecture based education. Not surprisingly, it found “the active learning intervention is superior as it works via three mechanisms, i.e. increased financial literacy, self-control, and financial confidence, while lecturing only affects financial confidence.”

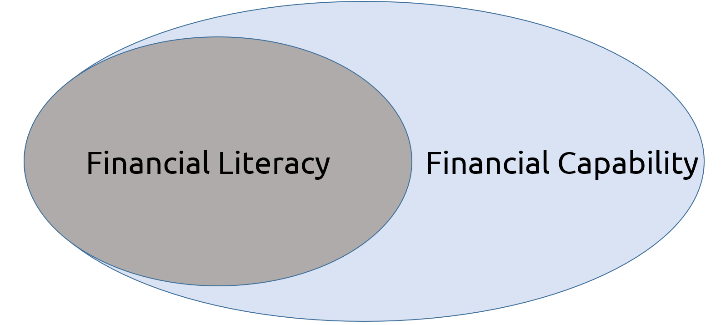

Increased expectations: financial literacy versus financial capability

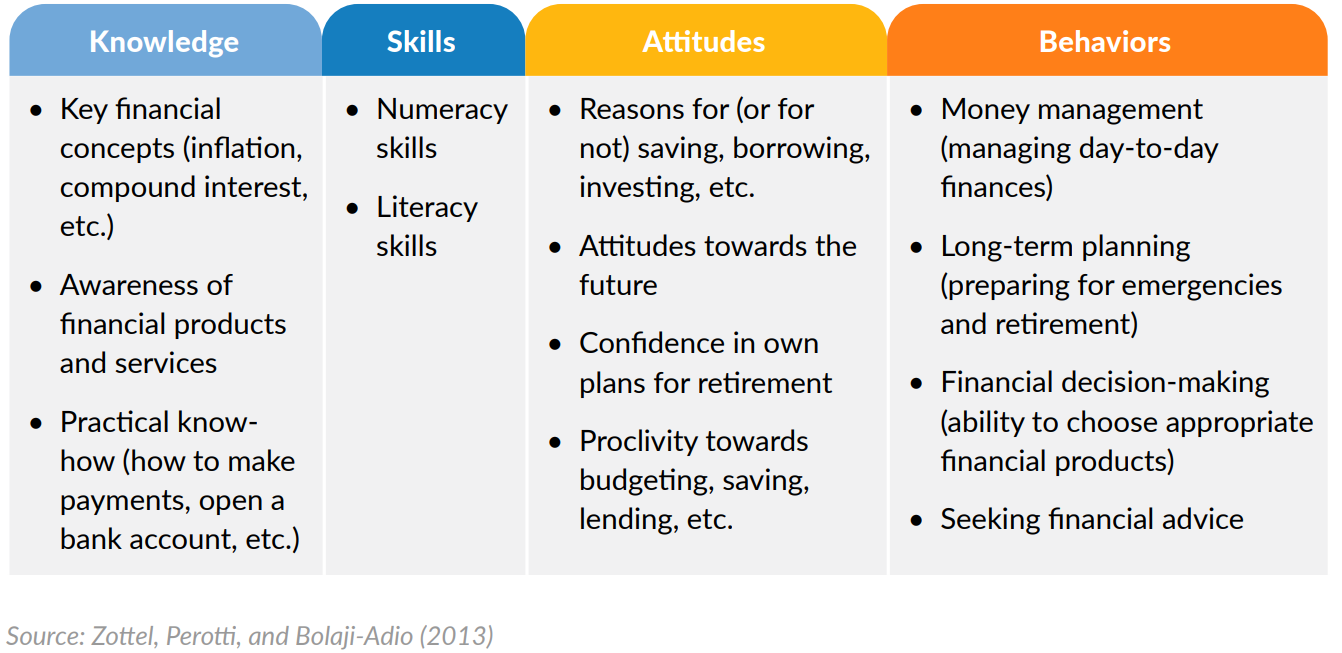

With the growing concern for young adults struggling financially and the increasing acceptance that more should be done, attitudes are changing regarding what is considered financial literacy. The recent report(2) by the Milken Institute documents the noticeable shift in expectations for what financial literacy must consist of in order to be effective. As we recognize that there is more to managing money than understanding concepts, the definition of financial literacy is expanding to include the skills, attitudes, and behaviors that together make up financial capability.

Knowing the significant differences between the effectiveness of interventions and the expanded definition of financial capability, educational leaders have key questions to consider.

What does effective education look like?

If we examine how core subjects are taught, we generally find three key components.

- Content is spiraled. Core subjects are repeated yearly over a long time period with prior learning providing the foundation for new learning.

- Curriculum is vetted and purchased. Before schools authorize purchases, there is typically a review process that involves a methodical evaluation by department leadership and curriculum coordinators. Free resources often circumvent this vetting process leaving the decision to the teacher’s discretion.

- Teachers are trained and certified in the subject they teach. Elementary educators are required to complete a cohort of classes in the core subjects while secondary educators typically have a major or minor in their area of certification.

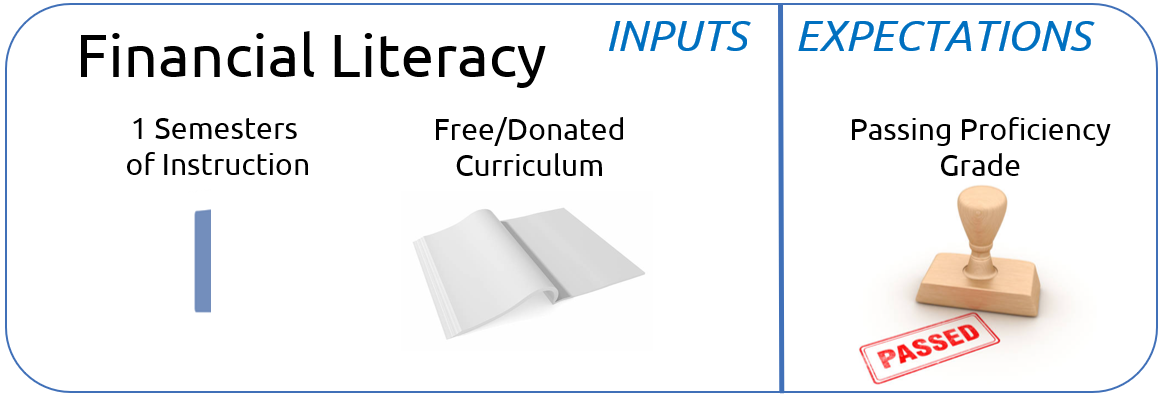

Below is an illustration of the cumulative educational inputs that core subjects are given with the educational expectation of students passing end-of-course or pre-graduation proficiency tests. While each state has some variability in requirements, this generally holds true for core subjects like English Language Arts (ELA), math, social studies, and science.

How does financial literacy education differ from successful core education?

There is wide variability in how financial literacy is taught, but in general, it is taught in a significantly different way than core subjects.

- One semester versus 20 to 26 semesters. Financial literacy is typically taught as a single semester class or as an add-on to an existing class such as economics or math.

- Usually relies on free curriculum. Unlike core subjects, individual teachers often have the responsibility of finding their own materials without a budget to purchase them. This results in teachers using free curriculum often provided by the same institutions that benefit from financial mistakes.

- Teachers lack formal preparation or certification. In a survey(3) of over 1200 teachers sponsored by the National Endowment for Financial Education, less than 20 percent reported feeling very competent to teach any of the six personal finance topics surveyed. Though alarming, this is not surprising, considering that no college or university in the United States offers a teacher certification or secondary education major in the subject.

Expectations far exceed what high schools have delivered, but should we be surprised?

The core subjects that do receive the 26 semesters of spiraled instruction, certified instructors and vetted curriculum are not expected to make life-long behavior and attitudinal changes or adult-level skills. So, it is realistic to expect even more from a subject like financial literacy that receives only a fraction of the inputs?

Core curriculum education versus CTE emphasis on hands-on learning

With a new focus on capability, it makes sense to review a successful educational model where the focus is to prepare students with the skills, attitudes, and behaviors necessary to be successful in an adult career. Career and Technical Education (CTE) classes are designed and implemented differently than core classes such as math, science, ELA, and social studies and is a model for effective financial education. How is CTE different?

- Courses are of significantly shorter duration. Most CTE classes last from two to four semesters with some classes being a single semester.

- Instruction emphasizes hands-on applied learning. CTE classes are offered in labs or skill centers and sometimes include off-site learning to provide students the opportunity to apply the concepts and skills learned in a setting similar to the workplace.

- A real-world assessment measuring capability is part of the program. CTE classes provide end-of-course certifications documenting proficiency, time-on-task, and measurable skills.

The innovation of hands-on applied learning and a financial capability test

“Simulation” is a word often used in education, but it has always meant something closer to an imaginative exercise. This innovation is the first ever true-to-life capability test, designed to highlight competing financial trade-offs, develop financial habits, and provide real time feedback that shapes behaviors and attitudes.

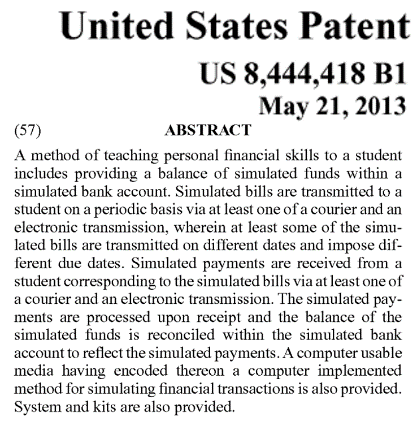

Budget Challenge patents numbers 8,444,418 and 8,740,617 describe a method of sending bills and reconciling payments across multiple due dates in an educational simulation. This innovation makes it possible for a student-centered real-time real-life financial simulation where students manage the finances of an independent young adult.

The patent represents only one of the many innovations contained in the Budget Challenge program. In combination, they produce the same results as effective CTE programs.

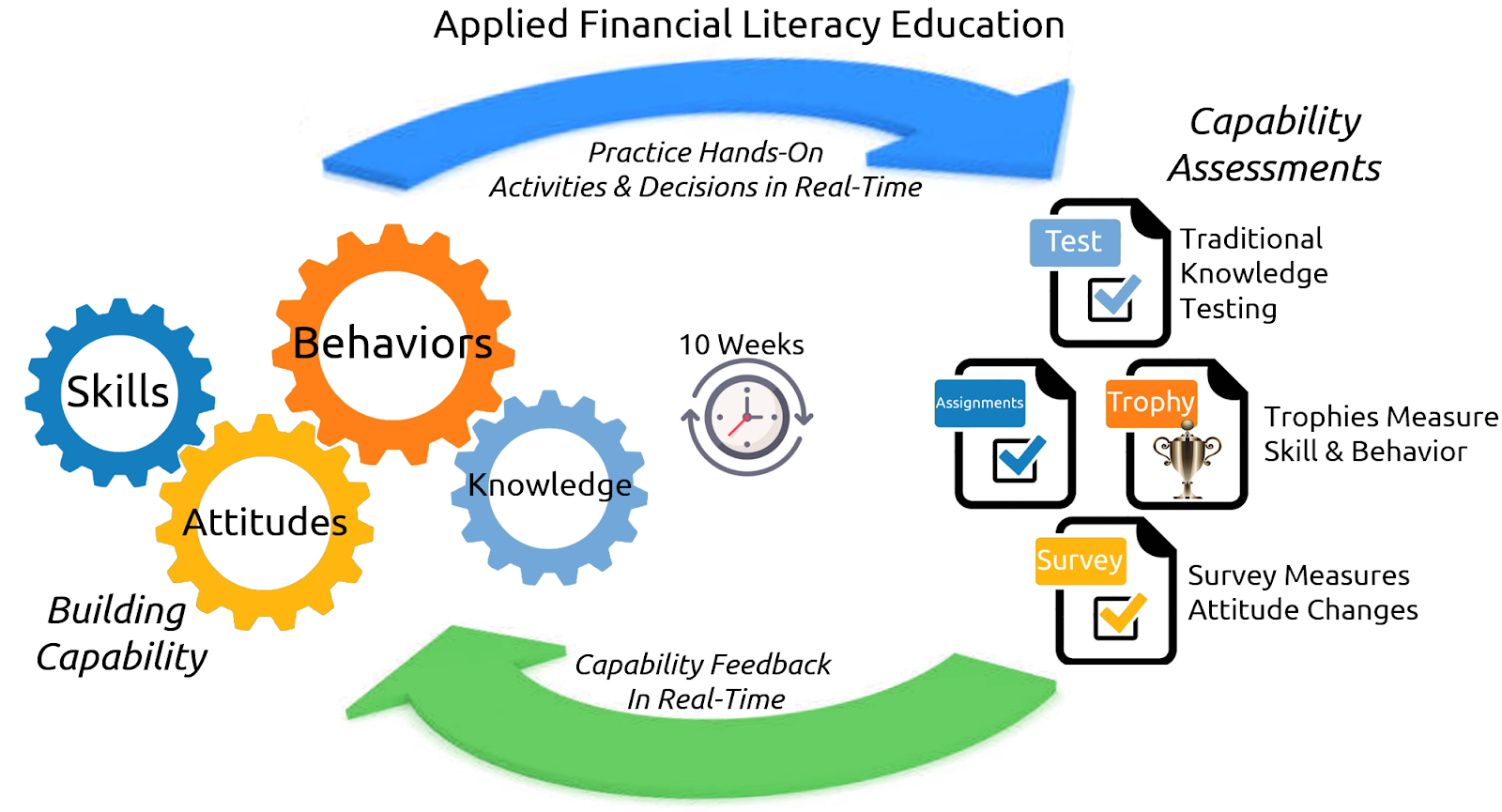

Developing Skills, Attitudes, Behaviors, and Knowledge

The expectations of financial capability mirror those of successful CTE programs. Regardless of the program, there is new knowledge and skills that must be learned. Because CTE is preparing students directly for the workforce and/or additional training, positive behaviors must be instilled as well. An example of this in CTE might be putting on appropriate safety gear or replacing equipment when finished with it.

In Budget Challenge positive behaviors include things like checking account balances before making payments, paying bills on time, paying down debt, and paying yourself first by having retirement contributions withheld from your paycheck. In a CTE class, positive attitudes might include treating patients with compassion or offering to assume additional responsibility. And, in Budget Challenge, students learn positive financial attitudes like recognizing the importance of a credit score and taking responsibility for one’s own financial future. Learning these things simultaneously results in them reinforcing each other creating synergy impossible when learning them separately.

Sustained practice builds deep knowledge and capability

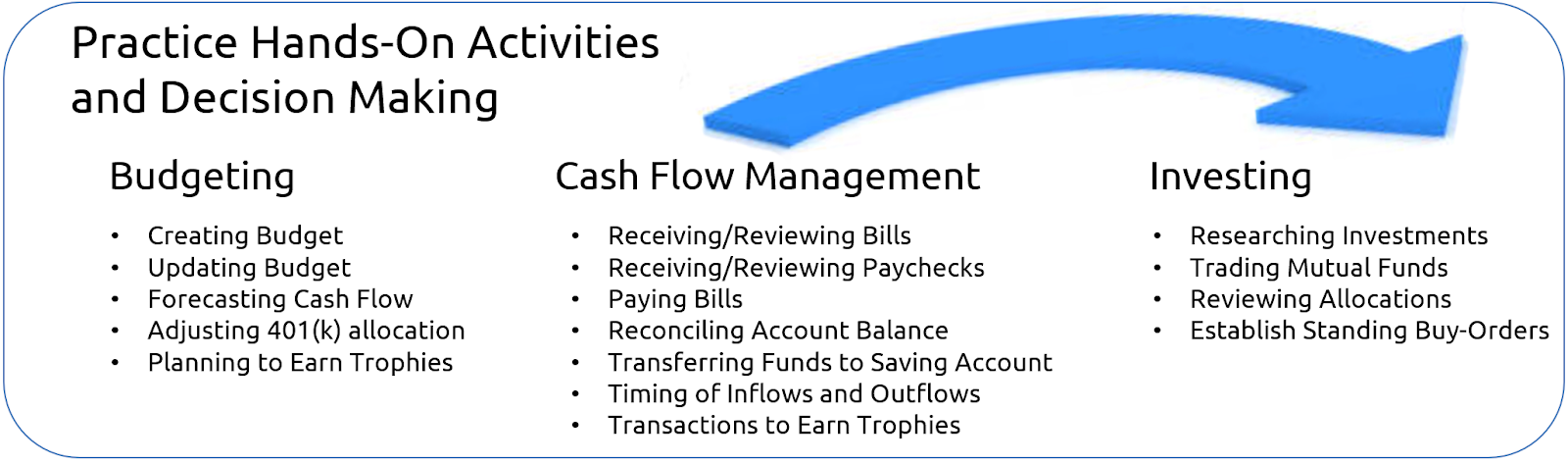

In order to build true capability students must have the opportunity to apply the knowledge and skills they learn in a real-life situation. In CTE this typically occurs in a lab, shop, or real-world setting. This application, practiced repeatedly, allows for the development of positive behaviors and attitudes. In Budget Challenge, students perform specific tasks and routinely engage in higher-order thinking and decision-making. It is through this process that students begin to understand how most financial decisions are interrelated and how actually managing finances is very different than simply reading about them.

In a typical CTE class, as much time or more is spent on practice as in the initial learning. This sustained practice allows for learning from mistakes, developing proficiency and performing skills in different circumstances. In Budget Challenge, students manage the finances of an independent young adult for ten weeks. This allows students to practice through multiple cycles of payroll, monthly bills, semi-annual bills, and an unexpected financial event. Like in CTE, they learn from their mistakes, experience different situations, and develop proficiency as well as the desired behaviors and attitudes.

Meaningful actionable feedback reinforces positive behaviors and improves performance

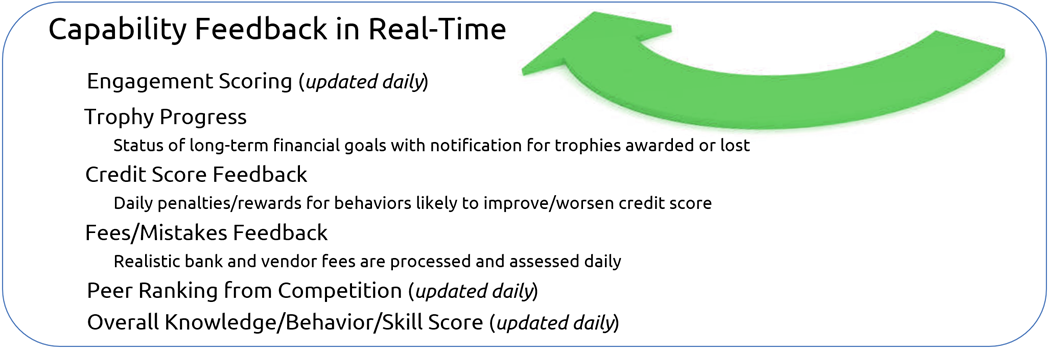

In CTE classes, effective feedback comes from many different sources but is always actionable. The feedback from making in error when building or constructing something, cutting someone’s hair, or welding a joint is often readily apparent to the student without intervention by the teacher. In other situations, the teacher provides feedback to help the student improve their performance. Research has shown that the most effective student feedback is timely, specific, and can be acted on. Budget Challenge automatically provides students with multiple types of meaningful feedback that shapes the behavior and learning. The program provides the teacher with multiple types of student performance data and automated tools to provide students with feedback that will help them learn.

Formative and summative assessments on the things that matter

CTE classes differ from many core classes in that students don’t just pass a written test to determine proficiency. They must demonstrate specific skills at a level of proficiency determined by real-world experience. So, a cosmetology student doesn’t gain certification solely from passing a written test. They must demonstrate they have the necessary skills. In addition, they are often required to successfully practice a specific number of hours to establish they also have the attitudes and behaviors necessary to be successful. As CTE students work towards their goals they receive formative assessment to increase their chance of success. If they successfully meet program goals, besides a grade, they often receive certification in their area of study.

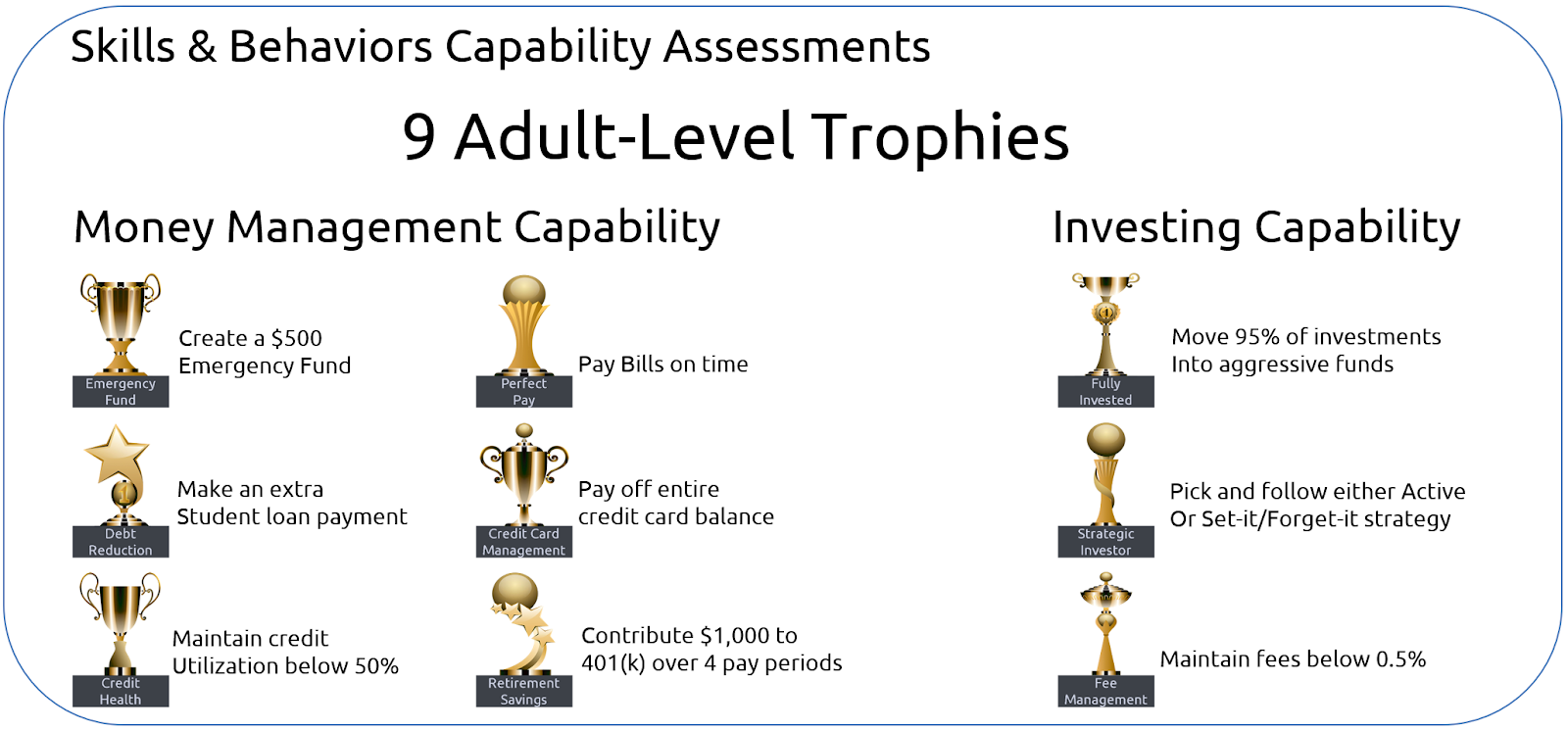

In Budget Challenge students attempt to earn trophies by demonstrating they can achieve financial tasks adults struggle with. Students receive daily formative feedback on their progress towards these trophy goals. Successfully accomplishing trophy goals are one of several types of summative feedback provided to students at the end of the simulation.

In addition to trophy goals, assignments, traditional knowledge testing, and surveys of attitude and behavior changes provide a comprehensive picture of what a student is learning during the simulation and at the end of the course.

Our program addresses the biggest shortcoming in financial education

Even the most engaging lessons about money fall short in one crucial aspect. By detaching the experience from the reality of managing finances they fail to teach the most important lessons. Most financial decisions involve trade-offs. In a simulation, it may be fun to invest $100,000 you’ve been “given” or learn how much interest can be saved by paying down debt. But in real life, most students won’t be given $100,000 to invest and in order to pay down debt, they must have money left over after paying current expenses. Money put in an emergency fund is money that can’t be used for a 401(k) match or to pay down credit card debt.

In real-life, decisions must be made while considering all other aspects of one’s finances. Evaluating trade-offs, managing cashflow, and setting priorities can only be meaningfully taught in a simulation that operates like the real world. Budget Challenge places these decisions in a simulation where students learn by managing ALL the finances of a typical independent young adult in real-time for ten weeks. The realism that makes the best CTE programs so effective is what makes Budget Challenge uniquely effective among financial literacy programs.

Supporting teachers with the best tools, customized training, and live help desk

As mentioned earlier, another challenge facing financial literacy education is the lack of teacher preparation. Budget Challenge closes the preparation gap by providing extended teacher play interactive training where teachers, like their students, learn by doing. Live webinars can be customized to meet teacher needs and schedules. Teacher support continues once school starts. Built-in teacher tools promote student engagement, identify struggling learners, assess progress, and extend the learning at home. A live professional Help Desk provides on-demand continuous support for both teachers AND students throughout their use of the program.

Evidence that Budget Challenge is effective using multiple measures of student performance

The following data shows effectiveness data that far surpass all other methods of teaching financial literacy. Results are not surprising when considering how the program overcomes the limitations and drawbacks of traditional financial literacy education.

Student performance on an assessment of financial knowledge and skills

Students were given pre and post-tests of core financial literacy and capability concepts and significant improvement was found.

Instilling positive financial habits and behaviors

Participating in Budget Challenge exemplifies active learning and the completion of multiple tasks requiring higher-order thinking skills. This results in increased retention compared to traditional financial education. It also results in the development of skills and positive financial behaviors and attitudes.

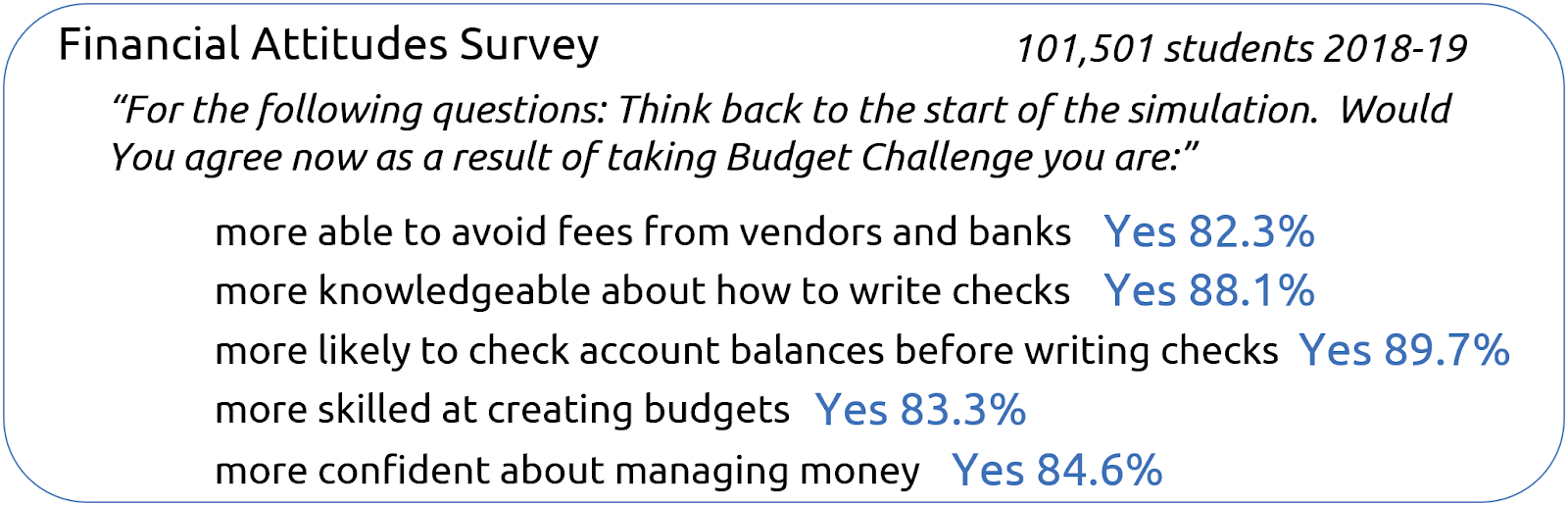

Students were asked to reflect on their learning and predict the impact the program had on their ability to perform important adult-level financial tasks.

Budget Challenge invites third-party analysis of our results and student data set

The data shown comes from large sample population sets from a wide range of schools representing broad geographic and socio-economic diversity. Budget Challenge is interested in working with any advocacy group or academics interested in researching the impact the program has on students.

References

- Kaiser, Tim, Annamaria Lusardi, Lukas Menkhoff, and Carly Urban. 2020. “Financial Education Affects Financial Knowledge and Downstream Behaviors.” https://gflec.org/wp-content/uploads/2020/04/Working-Paper-Financial-education-affects-financial-knowledge-and-downstream-behaviors-April_2020.pdf?x83489

- Contreras, Oscar, Joseph Bendix, 2021. Milken Institute “Financial Literacy in the United States” https://milkeninstitute.org/sites/default/files/2021-08/Financial%20Literacy%20in%20the%20United%20States.pdf

- Coggshall, Jane G, Lauren Bivona, Daniel J. Reschly. 2012. National Comprehensive Center for Teacher Quality “Evaluating the Effectiveness of Teacher Preparation Programs for Support and Accountability” https://files.eric.ed.gov/fulltext/ED543773.pdf