Welcome to this post about How to Manage Your Money as a Teenager!

Managing one’s money and having a solid grasp on the state of your finances is absolutely critical for all ages and all levels of wealth. The rich have a strong understanding of their finances and have organizational systems in place (if they don’t, they probably won’t be rich for long!). The poor, on the other hand, very likely have little to no understanding of where they are financially.

For example, Dave Ramsey’s Youtube channel abounds with countless videos of people making very silly financial mistakes, simply because they didn’t sit down and look at the numbers or were lacking in financial education – understandable since schools do not teach about money whatsoever. Therefore, it is totally up to the individual to educate themselves in this critical aspect of life.

If you’re interested in examples of the financial mistakes that can result from having a lack of clarity and organization, I highly recommend checking out Ramsey’s channel. Even if you don’t agree with his philosophy, at the very least, you’ll know which mistakes not to make! I’m sure you’ll find it both entertaining and educational.

I say all that to stress the absolutely critical importance of managing your money. It doesn’t matter if you are 7 or 70, you must do it. Granted, a seven-year-old’s system will be much simpler than a 70-year-old’s who is managing a retirement, but both are important.

The Benefits of Managing Your Money

When you tell your money where to go, plan what you’ll spend it on, and how much you’ll spend, save, and invest, only then will you be able to reach any of your financial goals, including financial independence and retirement. This critical cornerstone of financial intelligence, is the ABC’s of the money world. Without it, nothing else you do will work.

Want an example? Take the standard big bucks lottery winner. They’re our dream come true – bank accounts overflowing, striking it rich, and waking up the next morning with millions. The VAST majority of these “dreams come true” never end well. These winners end up broke, divorced, having lost all of their friends, and maybe even worse off than before in just a matter of a couple of years or less.

The moral of the story is this: If you’re bad with money now, with small amounts, you’ll be bad with it later, in much larger amounts (and end up burning yourself badly).

If you take nothing else from this, ask yourself:

- Do I know where, on what, and how much money I spend?

- Do I know how much I am saving and investing?

If you’ve got those two things under control you’ll be off to a great start. Simplistic, yes, but once you know these two things, you will have the clarity you need to move on to more advanced financial strategies. If needed, you can also start to look at how to cut expenses and save/invest even more.

The Basics of Managing Your Money

There are three general steps to managing your money. First, figuring out your income (as teens, this will be our biggest problem by far. If you have a regular job or stream of income, it will make it much easier). Second, finding your expenses, and lastly, how much you’re saving.

To explain the process, I’ll walk you briefly through my own situation.

1. Income

My parents started using Dave Ramsey’s “commission” method of chore compensation when I was about 8. I would get roughly $5 per week, plus the occasional $100-$150 in cash from friends and family on holidays and birthdays. I’ve always been a saver, so in a good year, I could accumulate about $500.

Just recently, at 16, I got my first job where I can earn about $250 every other week (depending on the number of shifts I sign up for). I still do basic required chores but for the most part, I’ve dropped the paid ones, and since holiday/birthday money is so varied, I’ll just leave that money out for now.

So, let’s go with a budget of $500 a month (Note: Wow. Ok, I’m not gonna say that you must work a part-time job, but if you get an offer for one, I strongly encourage you to TAKE IT. I don’t love my job, but oh boy do I love $500/month 😂).

2. Spending

From whenever you first start earning money to about the age of 16, this will be very simple. Personally, I never spent that much, so it was actually pretty boring trying to keep track of expenses! It’s not bad to spend money, but if you do, just make sure you keep track of it (which you’re learning how to do right now!), and save at least some.

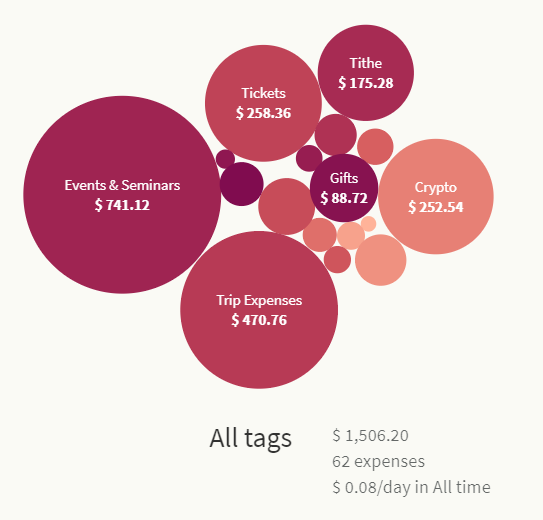

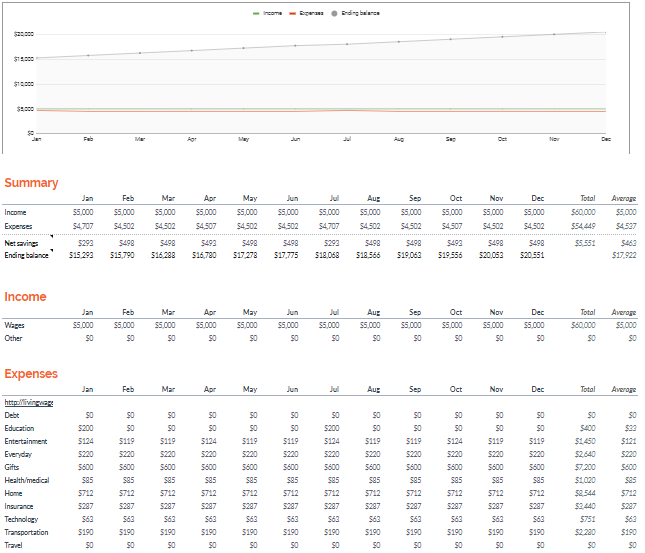

Now that I’ve turned 16, my expenses basically exploded. I started thoroughly tracking my money in February of 2019, and to date, I’ve already spent about $1,500 (it’s October 2019).

Woah, right? Normally, I would be appalled. “What on earth!?” Thankfully, since I’ve been tracking it, we can check and see where it’s all gone.

Right off the bat, you can see I’ve spent approximately 16% on savings and investments (the vast majority into crypto), 18% on charity/gifts, and a whopping 48% on seminars, travel, and tickets to seminars (if you add up the two biggest bubbles it appears to come to more than $1,200 but that’s because some expenses have multiple tags).

My three biggest categories add up to 82% of my spending. Were these expenses justifiable? I think so! Yes, I did spend a whopping amount on these events (and I’m nowhere near done lol), but that’s because of two reasons:

- My biggest focus for 2019 has been traveling to business seminars.

- This is my first event I’m funding completely on my own (flights, hotel, food, and Ubers. It’s not cheap) – no help from parents. Boy, I’m all grown up. 🙂

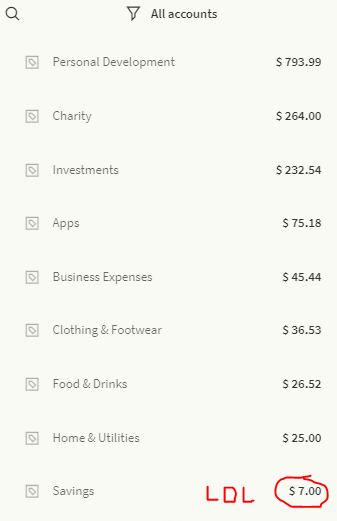

Still, that’s pretty weird and not what most teens would spend their entire years’ earnings on. I’ve spent $25 on my phone’s data plan, $26.52 on food and drinks (mostly with friends), and about $75.18 on app store purchases (ouchy). All these “frivolous” expenses together account for less than 1% of my spending for the year.

Summary: My total spending has tripled this year, but by tracking my expenses I can see that my “fun spending” has stayed roughly the same while “productive spending” has increased dramatically.

Again, without tracking it I probably would have spent much more on games and food. Something about manually logging what you’re spending money on makes you think twice about spending that money in the first place.

3. Saving/Investing

In prior years, this was where my focus was (and I was able to build up to about $1,500 invested in the stock market). I haven’t dropped that but, as I mentioned before, the majority of my focus this year has been saving up for events (specifically Unleash the Power Within this November). I have missed investing, though, so in 2020 it will be back on top as one of my number one priorities.

In the winter of 2018, a news article introduced me to cryptocurrencies. Shortly after, in the beginning of 2019, I joined a small investor group in my hometown. The group’s mentor posts updates specifically on crypto on a weekly basis. With his guidance, I’ve been dollar-cost averaging my way into several cryptocurrencies.

At the moment, I’m satisfied with my position and am done investing in crypto for a while (don’t want to put all my eggs in one basket). My next focus will probably be in real estate and the stock market.

Compared to my income, 2019 has been a pretty weak savings year for me. Though with the way it’s been going, and once I slow down on attending seminars, my goal is to get my savings/investing rate to above 50%, or even better, be able to max out my Roth IRA every year ($6,000).

Bringing It All Together

Now that I’ve defined my income, expenses, and savings rate (18%), going forward I can make actionable plans to increase my income and savings rate and redirect expenses to the most productive purchases possible and be able to see measurable progress.

So now it’s your turn! I highly encourage you to take an afternoon break and just jot down some of these numbers. If you’re a little older and have more expenses, then I encourage you even more so to look into getting a little more serious about it and creating a system for yourself.

Recommended Tools & Resources

I’m a bit of an extreme software nerd. It’s a personal hobby of mine to search high and low for coolest, slickest, and cheapest (better yet, free) financial software I can find. Here are some of the best money management ones I’ve found to date.

Toshl Finance

Toshl Finance is the one I personally use. It does have many paid features but the free ones work just fine for me. When my income is a little more consistent I’ll consider upgrading.

Pros:

- Free version

- In-depth graphs

- Extensive organization options (unlimited tags and categories)

- Extremely easy to find entries and compile summaries

- Accessible from computers, Apple Store, and Google Play Store

Cons:

- Locked premium features might get frustrating

- Too complicated

Personal Capital

Personal Capital is an extremely popular option. You can find many, many reviews of it online.

Pros:

- Extremely feature-rich

- Completely free (they make money by charging a fee if you sign up to use their professional investment managers)

- Tons of charts

- Budgets

- Net Worth compilation

- Automatically syncs your banking and investment accounts

- Accessible from computers, Apple Store, and Google Play Store

Cons:

- Buggy (the only reason I don’t use them right now is due to the fact that I’m constantly having problems linking my accounts. Ugh!)

EveryDollar

EveryDollar has been one I’ve used in the past and is still a favorite of mine. If you’re looking for strictly budgeting software, this is my absolute favorite.

Pros:

- Simple, clean, and very well designed

- Almost completely free

- If you’re a fan of Dave Ramsey, this was specifically designed for his methods by his company 😉

- Accessible from computers, Apple Store, and Google Play Store

Cons:

- Has one premium feature – syncing your bank account transactions for easy budgeting (to be honest, I think it’s completely worth the money)

- Might be too simple for some (including me, I’m a total data nerd… yet funnily enough I despise math. Yeah, explain that to me.)

Lastly, a Classic Spreadsheet

This is an extremely popular decision, though mostly among adults or finance nerds. I have a feeling the large majority of teens won’t find this option very appealing, but there are quite a few advantages to using a spreadsheet.

Pros:

- Infinitely customizable and personalized

- Completely free

- Synced and backed up in the cloud (if you use Google Sheets, I’m not sure how it works with excel), that means you can access it from your computer or the Google Sheets app

- Can be however simple or complicated you want it to be

- Hundreds of free budgeting templates online

Cons:

- Takes patience and some prior “spreadsheet skills” if you’re not already used to using them (I raged when I first started using spreadsheets at all 😂)

- Not very aesthetically pleasing (unless you invest a lot of time into making it so)

- Can get pretty complicated and confusing

The Takeaway

Wow! Thank you so much for sticking around. Hopefully, if you’ve made it this far, you were able to find some nuggets to apply in your personal life.

This entire article can be summed up in the following:

Managing your money properly is critical for financial success.

Your organizational system doesn’t have to be complicated and can be as simple as using your own homemade spreadsheet or signing up for EveryDollar. Any plan is better than no plan.

Check out more on this topic in the save money category!

For more information, check out the book: How to Manage Your Money: Control Your Money Before It Controls You.

I would love to hear your thoughts on the subject and if you already have any systems in place that have been working for you. Feel free to introduce yourself, and share your best tips with your fellow teens in the comments down below!

Also, a huge thanks to Jacob and Josh for giving me the opportunity to share on their site. They’ve got one of the best (and only, for that matter) teen money blogs I’ve found to date. Definitely give them and Teen Financial Freedom a follow!

Thanks for reading!