Welcome to How Much Should A Teenager Save From A Paycheck!

There are two main things you need to consider when figuring out your personal savings rate:

1. What are you saving for?

2. What and how much are your expenses?

What are you saving for?

Every situation is different, but most will need to save up for, at the very least, college expenses and their personal savings account (either a “rainy day fund” or a retirement account). Some teens will also need to save up for their own vehicle and all the expenses that come along with it. Others may also choose to save up for a house.

Getting your own vehicle is absolutely amazing and a huge step toward becoming independent, but if you can put off buying it at first, then I would do so. Cars are a massive expense and will easily eat into most of your earnings as a teen. Maintenance and insurance can chew through your earnings in no time. Still, if this is something you’ve been thinking about and preparing for, and you have your ideal car in mind (and you aren’t just getting it for the sake of saying you have a car), by all means, buy it!

What are your expenses?

As for the other factor, expenses, how much are they and what do they include? Some teens pay for their own cell phone bill or transportation, or already have a car and need to have money for insurance, gas, and repairs. Some will also likely have some entertainment expenses (money spent hanging out with friends or on video games).

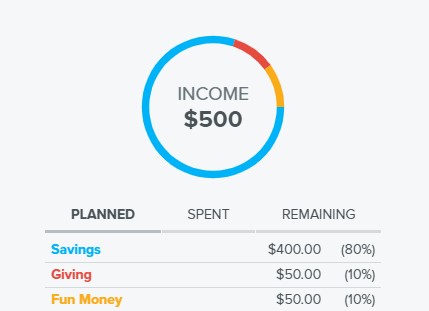

I’m going to be a little controversial here at first and state that if you have several items that you need to or want to save up for, then shoot for a savings rate of 80% (and a spending and giving rate of 10% each)

Note: Giving or tithe usually isn’t mentioned in the average teen’s budget, but I can assure you that it is not something to be underestimated and just cast aside. One of the best feelings in the world is setting aside money specifically for giving, and when you come across a situation where you can help someone out or put money towards a cause you’re passionate about, having the ability to be able to bless them financially without a second thought is amazing! Seriously, give it a try, even if you don’t start with 10% at first

How Much Of Your Paycheck Should You Save?

Now, you may be thinking, “Woah now! 80%?!? What about my social life? What about living? I don’t want to be a miser living on rice and beans and beans and rice!

I totally get you. That’s not the goal here. As a teen, these will be some of the free-est years in our entire lives and are the last ones we have before true adulthood, so I understand the desire to have fun (the fun doesn’t have to stop in adulthood, by the way (just ask my mom), though there are more responsibilities 😉)

Let me break it down for you. While, Yes, at first glance you’ll be setting aside 80%, it will be broken down into several categories of short-term and long-term savings.

For example, here is how I would break it down:

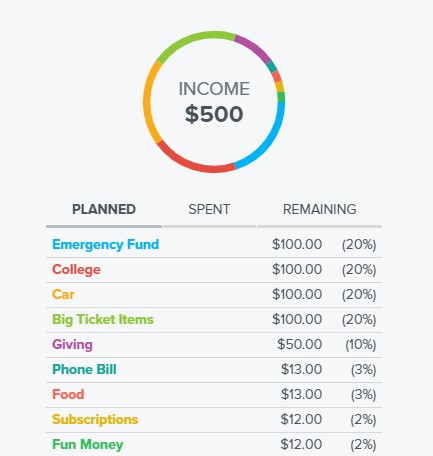

Example Budget:

- 80% Savings

- Investments/Emergency Fund (20%)

- College Expenses (20%)

- Buying a Car (and vehicle expenses) (20%)

- Other big-ticket items (a new computer, a gaming console, $300 Bose headphones, etc) (20%)

- 10% Fun Money and Expenses (entertainment, eating out, video games)

- 10% Tithe/Giving

This is completely customizable to your situation as well. Say you’ll be living in the dorms on your college campus and won’t need your own car right away. With 20% of your budget freed up, you could choose to split it among your other savings, save for a whole different item, or increase your “Fun Money” or giving budgets.

Also, your expenses might be to the point where they exceed 10% of your income already. As long as you aren’t spending like you’re in Congress, and it’s mostly going towards necessities (vehicle expenses for example), then that’s understandable.

The Size of Your Income

Your income also plays a large role. If you make $100 per month, your “Fun Money” budget would be $10 (savings would be $80 and giving would be $10). If you’re trying to cover a basic expense like a phone bill, $10 might not only not be enough, but then you wouldn’t have any “Fun Money” leftover… which would make for a pretty sad life, right?

In this case, it is understandable if you need to adjust the total savings rate to something like 70% or 60%. Don’t get too greedy though!

What the “Spending” category means:

I just want to make sure I clarify what this means. Not only does it include monthly “bills,” the spending category also includes any “fun” expenses or purchases you make. They’re usually smaller, cheaper purchases too. This could be a $10 Fortnite Battle Pass, buying a $5 bonus pack in one of your favorite games, spending a couple of bucks when you go out to eat with friends, or going to see a movie (do teens still do that? 😂).

I’m clarifying this because most of us won’t spend an absurd amount of money here (as long as you’re being reasonable and spending wisely). What I don’t include in the spending category are most bigger ticket items, like a gaming console, expensive headphones, a new phone or computer, or a super high-end pair of shoes (if it’s $100 or more, it’s probably a big-ticket item).

These items are accounted for with the 20% we set aside for “big-ticket items” in the budget I broke down above.

How Much Should A Teenager Save?

Learning to save as a teen or kid is literally one of THE most important things you could do. Get this: It doesn’t matter how much money you make. You could have a budget of $5 a week (like I did for several years). Teaching yourself to save even $2-$3 a week out of your $5 budget is just as powerful as saving $800 out of your $1,000 budget.

I’m dead serious. One of the most valuable things my parents ever gave me was this lesson right here. Around the age of 12 my siblings and I started earning chore money, and our only requirements were to save and tithe at least 10% each. More often than not, I ended up saving something close to 60% or 80% of that chore money.

Meticulously saving your hard-earned money and then reaching a milestone like $100 in savings is a feeling like no other.

Going with the Crowd

Your friends or peers might make fun of you for being so intentional with your money, especially when you refuse to spend your money on certain things. They might give you a weird look and tease you about it, but hold your ground.

Could you join them and decide to ignore all of this? Of course! Is it a good idea? Absolutely not. Just look at where the crowd is headed. When they’re 18 and step out of their parent’s house, they’ll have nothing. Nothing for college, nothing for their car, and nothing for emergency expenses. Pretty soon, all the fun at restaurants and blowing money with their friends will have to stop (or they’ll just go into debt), and their paychecks will be going towards just keeping afloat financially.

I haven’t experienced it firsthand, but I’m assuming the stress will also start to get to them pretty quickly, and they’ll be feeling like they aged a decade. And, oh, the regrets!

How Much Should I Save?

What if you decided to have the discipline and foresight to build the habit of saving money and to prepare for the future? College is waiting (for most but, keep in mind, not everyone!). Your car and all its lovely expensive quirks are waiting too. Old age isn’t going anywhere, and you’ll have to be able to take care of yourself later on.

Yeah, it’s a little weird talking about retirement when we haven’t even graduated high school, but let me just refer you to this article on the power of compound interest, and it’ll all make sense.

If you decided to set aside the majority of your paycheck while you were young and didn’t have dozens of expenses, you could get a massive head start on your peers. Unlike “the crowd,” imagine stepping out of your parent’s house at 18 having bought your own car, with a large cash emergency fund in the bank, and several thousand dollars saved up for college expenses. If you’re sticking to your budget, you can even still have fun!… Because you had the discipline to do the hard work first and put yourself in a position where you can still live life without breaking the bank.

How Much Money Should A Teenager Have?

Six in ten Americans say they would not be able to cover a $500 emergency expense (to put it into perspective, if you picked five random families from your school approximately three of them wouldn’t be able to cover a $500 emergency expense). If there’s one guarantee in life it’s that unexpected expenses will pop up.

27% of people said they would have to sell something or borrow money to cover the expense, and 12% would not be able to cover it at all. It’s honestly pretty sad that so many Americans are in such dire situations (and I’m sure people in other countries have similar situations). The stress alone knowing a random emergency could hit you at any time and you would be totally unprepared for it is pretty scary.

Learning to save at a young age might not seem very important since you most likely won’t be able to save a ton of money. Sure, it might only be a couple thousand dollars by the time you’re starting college, but it’s not just the money itself that is so important – equally as important or even more so is the habit you taught yourself.

Living Paycheck to Paycheck

78% of U.S. workers are living paycheck to paycheck. That means as soon as one paycheck comes in it’s spent almost immediately and they’re left desperately waiting for the next paycheck. 25% say they aren’t saving anything for retirement, and nearly 75% of them are in debt.

Almost always there are expenses they can cut back on and sacrifices they can make so that they can build an emergency fund and start paying off debt, but it is extremely stressful when you’re in the thick of it and it seems like there is no way you could save any money.

If you built the habit as a 16-year-old working your first job (or any age for that matter) of setting aside 10-20% for emergencies and your investment accounts, when you finish college and get your first job earning many times the amount you did as a teenager, the same principles apply.

Almost without a second thought, you start setting aside 10-20% of this much larger income for emergencies and your retirement and before you know it you have more than enough to cover a random $500 expense! The money was always there for someone living paycheck to paycheck, but it is much harder to see it. The coolest part of building the habit of saving early is it’s just that – a habit – so you never miss the money you’re saving.

The Takeaway

At the end of the day it is totally up to you and completely your decision. I know I probably have a pretty unconventional view since I believe it should be such a high savings rate, but I hope you were able to find some information or tips you’ll be able to use in your own life regardless if you’ll be saving 80% of your paycheck. 🙂

For an extra resource, check out: The No-Spend Challenge Guide: How to Stop Spending Money Impulsively, Pay off Debt Fast, & Make Your Finances Fit Your Dreams.

Constructive criticism and feedback is always welcomed! Feel free to comment below or share with a friend.

Don’t forget to check out some of Teen Financial Freedom’s other posts from our amazing team of writers! Thanks for reading!